mortgage refinance fees and how to keep them low

You pause at the kitchen table, disclosures open, and decide the savings must be worth the hassle. To make it convenient and safe, you compare itemized refinance closing costs, ask about a no-closing-cost refinance, and check how cash-out refinance fees change the math. Realistic check: some "costs" are escrow prepaids, not fees.

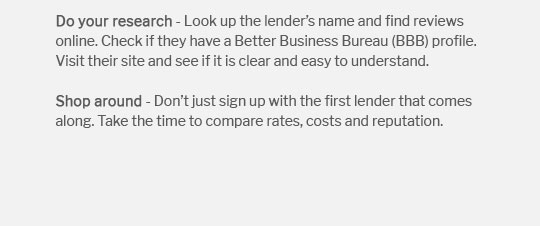

What to watch

- Origination, appraisal, title, recording: negotiate or shop; junk fees are optional.

- Rate trade-off: lender-paid credits lower cash due but raise the rate.

- Convenience and safety: secure uploads, e-signing, and a clear rate lock.

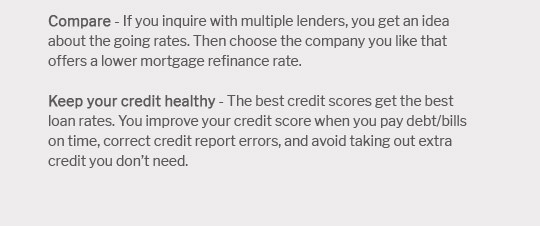

Smart steps to save

- Use a break-even refinance calculator; aim to recoup in 24 - 36 months.

- Compare APR vs interest rate on a rate-and-term refinance across three lenders.

- Time the appraisal and payoff to avoid extra per-diem interest and re-locks.

With clarity on fees and a calm plan, you refinance once, save steadily, and sleep better.